Indian equity benchmarks continued their uptrend, forming a higher high–higher low pattern for the second consecutive week ended April 17, despite volatility driven by West Asia tensions, fluctuations in oil prices, and March quarter earnings. Falling oil prices below $100 per barrel, amid hopes of a resolution to the Iran conflict and emerging ceasefire frameworks, supported the equity markets.

The strengthening rupee against the US dollar, valuation comfort, and a recovery in FII flows also boosted market sentiment. Encouragingly, the IMF raised India's FY27 GDP growth forecast to 6.5 percent from the previously projected 6.4 percent, even as it flagged global recession risks, highlighting India's macroeconomic resilience.On Monday, the market will first react to HDFC Bank and ICICI Bank's quarterly numbers, as well as the closure of the Strait of Hormuz and hope of second round of peace talks before ceasefire deadline of April 22. Going ahead, market direction in the coming week is expected to be driven by progress in peace talks, developments in the Strait of Hormuz, crude oil prices, FII sentiment, and March quarter earnings. The overall trend is likely to remain positive, despite expected volatility linked to a potential US-Iran deal.In the past week, the Nifty 50 soared 303 points (1.26 percent) to 24,354, while the BSE Sensex surged 943 points (1.22 percent) to 78,494, in addition to the nearly 6 percent rally seen in the previous week.

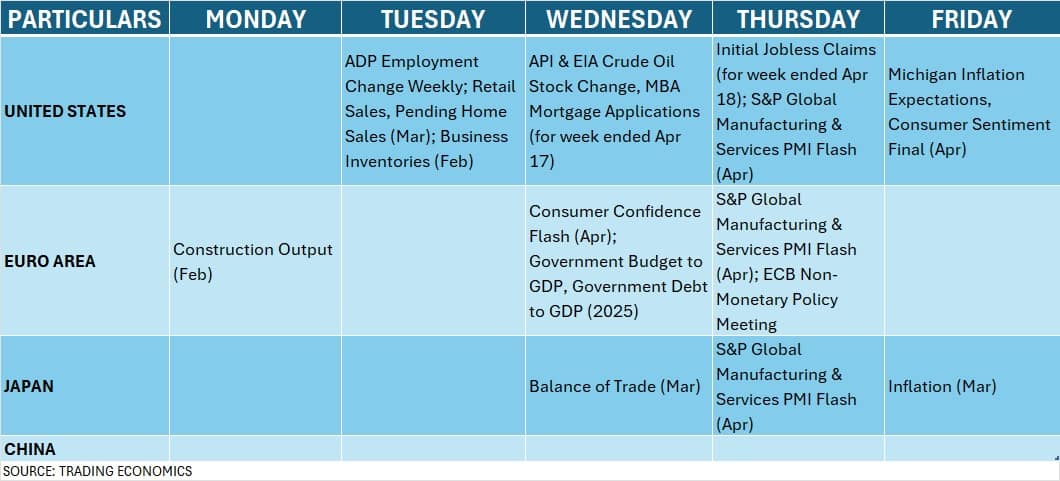

The broader markets outperformed the benchmark indices, with the Nifty Midcap 100 and Smallcap 100 indices gaining 3.55 percent and 4.3 percent, respectively.According to Vinod Nair, Head of Research at Geojit Investments, the near-term market direction hinges on progress in Middle East peace efforts, crude oil stability below $100, and the trajectory of foreign inflows.He added that sustained de-escalation could ease inflation and currency pressures, thereby improving risk appetite for import-sensitive markets like India. He also noted that Q4 earnings and FY27 management guidance will shape sectoral leadership.He believes that sentiment remains constructive, but markets will stay selective amid lingering global uncertainties.According to Siddhartha Khemka, Head of Research (Wealth Management) at Motilal Oswal Financial Services, equities are likely to consolidate at higher levels next week after a sharp 10 percent rally over the past ten trading sessions.Broader markets are expected to continue outperforming, aided by sector-specific news flows and Q4 earnings driving stock-specific action, he said.Here are 10 key factors to watch current week:Strait of Hormuz, Peace Talks Progress, Crude Oil PricesThe Strait of Hormuz and ongoing peace talks, along with the approaching ceasefire deadline on April 22, will be important factors for global investors to watch, particularly for their impact on oil prices. Equity markets have shown a healthy recovery over the last couple of weeks, with the Nifty 50 surging nearly 10 percent from its April low and US markets hitting record highs amid rising hopes of a resolution to the Iran conflict.After failing to reach an agreement in the first round of peace talks between US and Iran negotiators on April 12, market participants are now awaiting the second round of discussions. In a post on Truth Social, Trump said, “My Representatives are going to Islamabad, Pakistan — They will be there tomorrow evening, for Negotiations.” While CNN reported that Iranian sources say they are sending a team too.The Strait of Hormuz, a crucial waterway that handles around 20 percent of the global oil supply, remains the most critical factor in any potential US-Iran deal. On Friday, Iran reopened the waterway for commercial ships, triggering a relief rally in US markets and pushing oil prices down by 10 percent intraday. However, on Saturday, Tehran reimposed restrictions on the Strait, citing US “breaches of trust.” Additionally, Islamic Revolutionary Guard Corps (IRGC) gunboats fired on a transiting tanker (though the tanker and crew were safe), prompting several vessels to turn back.With the situation in the Strait of Hormuz still unresolved and the US blockade of Iranian ports continuing, attention will remain focused on how global markets and crude oil prices react in the coming week.Brent crude prices, the international oil benchmark, corrected by more than 12 percent intraday to $86.09 per barrel on Friday before recovering slightly to close at $92.41, down 5.9 percent for the day. For the week, prices declined by 1.95 percent, following a 13.71 percent drop in the previous week, but still remained above all key moving averages. Therefore, volatility is likely to persist in the coming week. However, prices need to fall below and sustain under $75 per barrel to provide meaningful relief to oil-importing nations such as India.Global Economic DataOn the global front, US retail sales, pending home sales, weekly jobless claims and Michigan inflation expectations will be closely tracked by the market participants globally for further signals on consumer resilience, alongside flash PMI readings from major global economies. Fed Chair Congressional TestimonyApart from economic releases, market participants across asset classes will also watch the incoming Fed Chair Kevin Warsh's congressional testimony scheduled on April 21, for early signals on the direction of US monetary policy. This is his first testimony since nomination as Fed Chair by the President Donald Trump.

Fed Chair Congressional TestimonyApart from economic releases, market participants across asset classes will also watch the incoming Fed Chair Kevin Warsh's congressional testimony scheduled on April 21, for early signals on the direction of US monetary policy. This is his first testimony since nomination as Fed Chair by the President Donald Trump.

Fed Chair Congressional TestimonyApart from economic releases, market participants across asset classes will also watch the incoming Fed Chair Kevin Warsh's congressional testimony scheduled on April 21, for early signals on the direction of US monetary policy. This is his first testimony since nomination as Fed Chair by the President Donald Trump.March Quarter Earnings

Back home, the focus will remain on further set of quarterly earnings scheduled next week. More than 90 companies will release their quarterly numbers in the next six days including Nifty 50 names like Reliance Industries, Infosys, HCL Technologies, Axis Bank, Nestle India, SBI Life Insurance Company, Tech Mahindra, Trent, and Shriram Finance which have more than 22 percent weightage in the benchmark index.Among others, IndusInd Bank, Billionbrains Garage Ventures Groww, Tata Elxsi, L&T Technology Services, Bank of Maharashtra, PNB Housing Finance, Central Mine Planning & Design Institute, Persistent Systems, Powerica, Bharat Coking Coal, Havells India, Tata Communications, Aditya Birla Sun Life AMC, Adani Energy Solutions, Cyient, Indian Energy Exchange, Sterling and Wilson Renewable Energy, Tata Capital, Tata Teleservices (Maharashtra), UTI Asset Management Company, Adani Green Energy, L&T Finance, Mahindra & Mahindra Financial Services, IDFC First Bank, and India Cements will also announce their quarterly earnings scorecard in the coming week.Domestic Economic DataEconomic releases like infrastructure output for March scheduled on April 20, HSBC Manufacturing & Services PMI Flash numbers for current month on April 23, and foreign exchange reserves for week ended April 17 will also be watched. Minutes of RBI monetary policy held in earlier this month will also be released next week on April 22.Manufacturing PMI dropped to 53.9 in March from 56.9 in February due to slow growth in factory output and new orders, while the services PMI during the same period also fell to 57.5 from 58.1.Meanwhile, foreign exchange reserves continued to trend higher for second consecutive week ended April 10 at US$700.95 billion from US$697.12 billion in previous week, especially after consistently falling for a month following the beginning of Iran war.FII Flow

The focus will also be on the mood at the Foreign Institutional Investors' (FIIs) desk as they provided sigh of relief in the recent week due to buying in last three straight sessions, though they turned net sellers to the tune of around Rs 251 crore worth shares for the week, the lowest selling after several weeks. They sold more than Rs 1.61 lakh crore worth shares since March, and over Rs 2.09 lakh crore in current year in the cash segment.FIIs buying in last three days amid the hope of potential West Asia war resolution, stability in rupee, and falling oil prices may be an indication of change in their mood. Follow-up buying interest from them is necessary for strengthening healthy trend in the market.On other side, Domestic Institutional Investors (DIIs) turned net sellers after a long time, offloading shares worth nearly Rs 6,300 crore in the passing week, which may be due to profit booking. They had bought Rs 2.8 lakh crore worth shares in current year and nearly Rs 30,000 crore in current month, providing strong support to the market in every fall.Indian RupeeThe movement in the Indian rupee will also be watched as the currency remained range-bound for last couple of weeks, especially after hitting record low of 95.22 against the US dollar and strengthening by 2.2 percent in the week ended April 2. In the recent week, it gained 0.51 percent to finish at 92.57 against the US dollar but has not breached all key moving averages yet.US dollar index softened for third straight week to 98.22 from 100.64 as improving sentiment around US–Iran de-escalation talks reduced safe-haven demand for the dollar, which along with the recent FIIs buying interest and cooling oil prices (that eased pressure on India's import bill) supported the rupee."Overall, the rupee remains supported in the near term, but sustainability will depend on the outcome of geopolitical developments and crude price stability," Jateen Trivedi, VP Research Analyst - Commodity and Currency at LKP Securities said.IPO Action

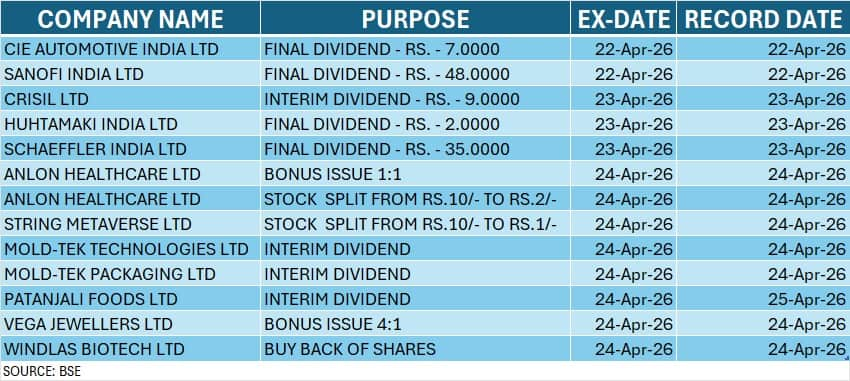

The IPO action has not seen strong revival action yet though the market sentiment has been improving for last couple of weeks. Leapfrog Engineering Services, from the SME segment, will be the only IPO hitting Dalal Street next week on April 23. The company is raising Rs 88.5 crore via IPO at the upper end of price band of Rs 21-23 per share.Citius Transnet Investment Trust, and Mehul Telecom will close their public issues on April 21, while Property Share Investment Trust's Propshare Celestia and Mehul Telecom will make their debut on the BSE on April 24.Technical View, F&O Cues, VIXTechnically, the momentum in the near term remains in favour of bulls with the RSI climbing to over 57 and the MACD reaching closer to zero line with expansion in histogram green bar, while the index sustained well-above short term moving averages which both trended upward. Now, the Nifty 50 needs to convincingly break above 24,400, the recent week's high, for sharp upmove toward 24,700-24,800 as above it 25,000 is the level watch going ahead, while the immediate support is placed at the 24,200-24,100, followed by 23,900 as a crucial support.The weekly options data indicated that the Nifty 50 is expected to be in the 24,000-24,800 range in the upcoming sessions, while the broader range could be 23,800-25,000. The maximum Call open interest was placed at the 25,000 strike followed by the 24,800 and 24,500 strikes, with the maximum Call writing at the 25,000, 25,050 and 24,600 strikes. On the Put side, the 24,000 strike holds the maximum open interest followed by the 24,200 and 23,800 strikes, with the maximum Put writing at the 24,000, 24,300 and 24,200 strikes.Meanwhile, the fear index India VIX fell 8.73 percent to 17.2, extending downtrend for third consecutive week from more than 21-month high of 28.9, signalling comfort for bulls. Falling further toward 14 zone can provide more support to the bulls.Corporate ActionHere are key corporate actions taking place in the coming week: Report prepared by Mr Sunil Sankar Matkar of Network18

Report prepared by Mr Sunil Sankar Matkar of Network18

Back home, the focus will remain on further set of quarterly earnings scheduled next week. More than 90 companies will release their quarterly numbers in the next six days including Nifty 50 names like Reliance Industries, Infosys, HCL Technologies, Axis Bank, Nestle India, SBI Life Insurance Company, Tech Mahindra, Trent, and Shriram Finance which have more than 22 percent weightage in the benchmark index.Among others, IndusInd Bank, Billionbrains Garage Ventures Groww, Tata Elxsi, L&T Technology Services, Bank of Maharashtra, PNB Housing Finance, Central Mine Planning & Design Institute, Persistent Systems, Powerica, Bharat Coking Coal, Havells India, Tata Communications, Aditya Birla Sun Life AMC, Adani Energy Solutions, Cyient, Indian Energy Exchange, Sterling and Wilson Renewable Energy, Tata Capital, Tata Teleservices (Maharashtra), UTI Asset Management Company, Adani Green Energy, L&T Finance, Mahindra & Mahindra Financial Services, IDFC First Bank, and India Cements will also announce their quarterly earnings scorecard in the coming week.Domestic Economic DataEconomic releases like infrastructure output for March scheduled on April 20, HSBC Manufacturing & Services PMI Flash numbers for current month on April 23, and foreign exchange reserves for week ended April 17 will also be watched. Minutes of RBI monetary policy held in earlier this month will also be released next week on April 22.Manufacturing PMI dropped to 53.9 in March from 56.9 in February due to slow growth in factory output and new orders, while the services PMI during the same period also fell to 57.5 from 58.1.Meanwhile, foreign exchange reserves continued to trend higher for second consecutive week ended April 10 at US$700.95 billion from US$697.12 billion in previous week, especially after consistently falling for a month following the beginning of Iran war.FII Flow

The focus will also be on the mood at the Foreign Institutional Investors' (FIIs) desk as they provided sigh of relief in the recent week due to buying in last three straight sessions, though they turned net sellers to the tune of around Rs 251 crore worth shares for the week, the lowest selling after several weeks. They sold more than Rs 1.61 lakh crore worth shares since March, and over Rs 2.09 lakh crore in current year in the cash segment.FIIs buying in last three days amid the hope of potential West Asia war resolution, stability in rupee, and falling oil prices may be an indication of change in their mood. Follow-up buying interest from them is necessary for strengthening healthy trend in the market.On other side, Domestic Institutional Investors (DIIs) turned net sellers after a long time, offloading shares worth nearly Rs 6,300 crore in the passing week, which may be due to profit booking. They had bought Rs 2.8 lakh crore worth shares in current year and nearly Rs 30,000 crore in current month, providing strong support to the market in every fall.Indian RupeeThe movement in the Indian rupee will also be watched as the currency remained range-bound for last couple of weeks, especially after hitting record low of 95.22 against the US dollar and strengthening by 2.2 percent in the week ended April 2. In the recent week, it gained 0.51 percent to finish at 92.57 against the US dollar but has not breached all key moving averages yet.US dollar index softened for third straight week to 98.22 from 100.64 as improving sentiment around US–Iran de-escalation talks reduced safe-haven demand for the dollar, which along with the recent FIIs buying interest and cooling oil prices (that eased pressure on India's import bill) supported the rupee."Overall, the rupee remains supported in the near term, but sustainability will depend on the outcome of geopolitical developments and crude price stability," Jateen Trivedi, VP Research Analyst - Commodity and Currency at LKP Securities said.IPO Action

The IPO action has not seen strong revival action yet though the market sentiment has been improving for last couple of weeks. Leapfrog Engineering Services, from the SME segment, will be the only IPO hitting Dalal Street next week on April 23. The company is raising Rs 88.5 crore via IPO at the upper end of price band of Rs 21-23 per share.Citius Transnet Investment Trust, and Mehul Telecom will close their public issues on April 21, while Property Share Investment Trust's Propshare Celestia and Mehul Telecom will make their debut on the BSE on April 24.Technical View, F&O Cues, VIXTechnically, the momentum in the near term remains in favour of bulls with the RSI climbing to over 57 and the MACD reaching closer to zero line with expansion in histogram green bar, while the index sustained well-above short term moving averages which both trended upward. Now, the Nifty 50 needs to convincingly break above 24,400, the recent week's high, for sharp upmove toward 24,700-24,800 as above it 25,000 is the level watch going ahead, while the immediate support is placed at the 24,200-24,100, followed by 23,900 as a crucial support.The weekly options data indicated that the Nifty 50 is expected to be in the 24,000-24,800 range in the upcoming sessions, while the broader range could be 23,800-25,000. The maximum Call open interest was placed at the 25,000 strike followed by the 24,800 and 24,500 strikes, with the maximum Call writing at the 25,000, 25,050 and 24,600 strikes. On the Put side, the 24,000 strike holds the maximum open interest followed by the 24,200 and 23,800 strikes, with the maximum Put writing at the 24,000, 24,300 and 24,200 strikes.Meanwhile, the fear index India VIX fell 8.73 percent to 17.2, extending downtrend for third consecutive week from more than 21-month high of 28.9, signalling comfort for bulls. Falling further toward 14 zone can provide more support to the bulls.Corporate ActionHere are key corporate actions taking place in the coming week:

Report prepared by Mr Sunil Sankar Matkar of Network18 Disclaimer: The views and investment tips expressed by experts are their own. We advise readers and Investors to check with certified experts before taking any investment decisions.

No comments:

Post a Comment