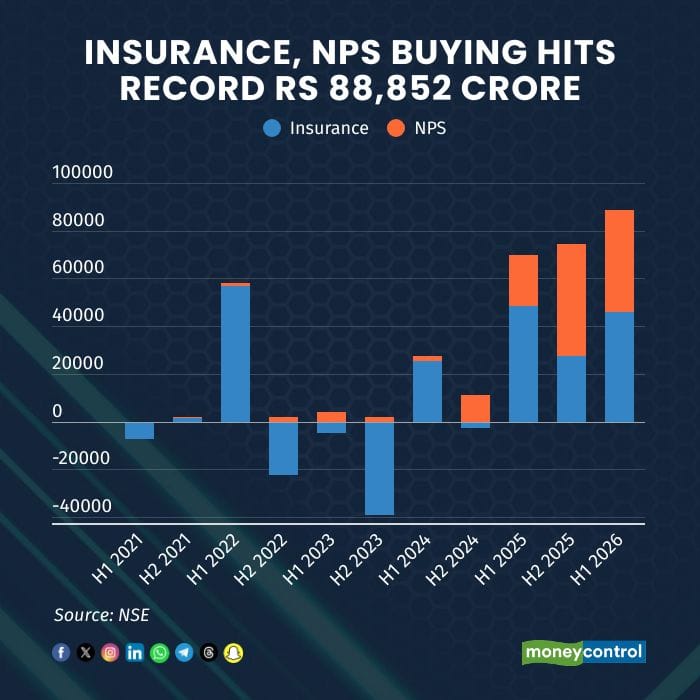

During January-June 2026, insurance companies bought equities worth around Rs 45,929 crore while NPS bought around Rs 42,922 crore, taking combined six-month buying to Rs 88,852 crore, a record since data became available in 2021, NSE data showed. Both insurance and NPS have seen robust, continued investment in Indian markets since the start of 2025, with combined buying of Rs 69,900 crore in the first half of the year and Rs 74,413 crore in the second half.

Raj Gaikar, Equity Research Analyst at SAMCO Securities, said the key driver behind these inflows is the nature of the capital itself. Unlike foreign portfolio flows, insurance premiums and NPS contributions are long-term and recurring, meaning investments continue irrespective of short-term market movements. Insurance companies receive a steady stream of premium income, while NPS benefits from regular monthly contributions from a rapidly expanding subscriber base, so neither is attempting to time the market.

Raj Gaikar, Equity Research Analyst at SAMCO Securities, said the key driver behind these inflows is the nature of the capital itself. Unlike foreign portfolio flows, insurance premiums and NPS contributions are long-term and recurring, meaning investments continue irrespective of short-term market movements. Insurance companies receive a steady stream of premium income, while NPS benefits from regular monthly contributions from a rapidly expanding subscriber base, so neither is attempting to time the market.In January-June 2026, India's benchmark Sensex and Nifty fell 10 percent and 8.66 percent respectively, while the broader BSE MidCap 150 and BSE SmallCap 250 indices gained 1.4 percent and 5.5 percent respectively. The year saw significant volatility on account of stretched valuations, continued FII selling, and trade tensions. The recent conflict involving the US, Iran and Israel triggered a surge in crude oil prices and weakened macroeconomic conditions.Though Indian markets have recovered since the start of April, returns for the year remain muted, creating what some see as an attractive opportunity for these institutions to accumulate quality companies at more reasonable valuations. A gradual shift in household savings away from traditional assets such as bank deposits and gold towards market-linked investment products has further strengthened this domestic liquidity.Behind the steady flows lie two structural reasons why this money keeps coming regardless of returns. From a regulatory standpoint, insurers operate under prudent investment norms that require a significant portion of their traditional funds to remain invested in government and other approved securities, with diversification limits on individual companies.For insurance, a parallel effect plays out through product mix — ULIPs and market-linked pension plans are taking share from traditional endowment products, and equity allocation follows the product design automatically. Nobody at an insurer is making a market call in this process; the policyholder picks the plan, and the fund manager simply executes it.For NPS, the Active Choice option permits equity allocation of up to 75 percent, while the Multiple Scheme Framework introduced in October 2025 allows eligible non-government subscribers to opt for schemes with equity exposure of up to 100 percent, depending on their investment preference. That marks a meaningful shift from a few years ago, when the scheme was structurally debt-heavy. Combined with a growing subscriber base contributing every month through payroll, this produces equity buying that is largely indifferent to how the index performed the previous week — it is contractual rather than discretionary in nature.Set against a year in which FIIs have remained on the sidelines, selling nearly $29 billion so far in 2026, these two sources of demand have created something Indian markets have not had before at this scale — a genuinely domestic, contribution-driven demand base that is not performance-chasing. Mutual funds have added over Rs 2.88 lakh crore so far in 2026, taking total domestic institutional investor (DII) investment to around Rs 4.64 lakh crore so far this year. That, market participants say, is the real support level under Indian equities right now.Atish Jain, CEO of Choice Connect, a partner-led financial distribution platform, said anyone building a five-year thesis on India should stop treating FII flows as the swing factor they once were. NPS penetration remains low relative to the size of the workforce, insurance's share of savings is still growing, and neither trend depends on stock returns to keep expanding. A flat year like this one, he said, is a stress test that the structure is passing quietly.

written by Ravindra Sonavani,

Source: Network18

No comments:

Post a Comment