For years, diagnostic chains were built on pathology: asset-light, high volumes, low ticket sizes, and predictable cash flows. That model is now shifting towards radiology, which is steadily becoming the revenue engine.

Full-body scans, cancer screenings, and cardiac imaging are becoming more common. Radiology is central to this trend because imaging enables early detection. With higher realizations, operating leverage, and deeper clinical relevance, Radiology is altering the growth trajectory. An asset-heavy business model also creates an entry barrier.

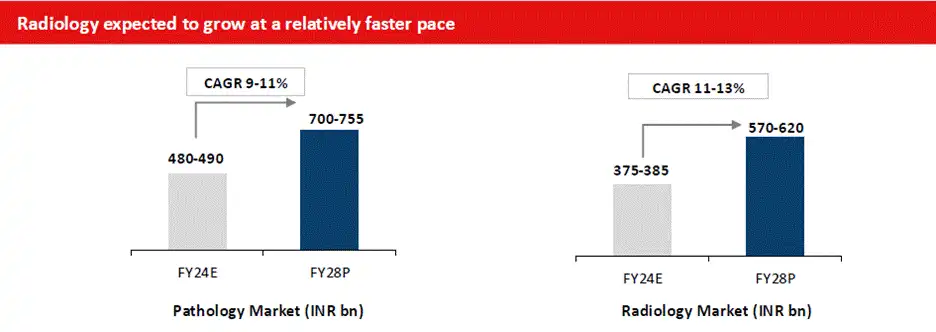

Radiology Market to Grow at 11-13% CAGR

Source: Suraksha Investor Presentation

Source: Suraksha Investor Presentation

Consequently, the broader Indian radiology market is expected to grow faster than the pathology market at 11-13% CAGR between FY24 and FY28. The market size is expected to reach around ₹62,000 crore by then, according to Suraksha Diagnostic. On a similar note, let’s take a look at three pathology players with a high radiology revenue-mix.

#1 Vijaya’s Radiology business has built an impenetrable moat

Vijaya Diagnostic Centre is India’s largest integrated, direct-to-consumer (B2C) diagnostic chain. The company has evolved from a regional leader into a massive network of 162 state-of-the-art centers spread across 27 cities and towns in India. B2C generates about 92% of its revenue.

Regional expansion strategy

Hyderabad remains the key geographic area, contributing 68-69% of revenue. To strengthen its foothold, it recently opened new hubs in regional markets, including Khammam (Telangana) and Nandyal (Andhra Pradesh). It is also expanding into West Bengal and Bengaluru.

Revenue-Mix

Source: Vijaya Investor Presentation

The radiology segment is a core pillar of its integrated B2C business model. The company offers two diagnostic verticals: Pathology and Radiology. The pathology segment consistently accounts for 63% of total revenue, while the radiology segment accounts for the remaining 37%.

Dominance in Radiological technology

Vijaya has been a pioneer in radiological technology. It is the first independent diagnostic center in South India to offer PET CT scans and the first in Telangana to purchase a 50-slice CT scanner. Today, its radiology infrastructure includes 43 MRI machines, 41 CT machines, and 9 gamma machines.

The company claims that its radiology operations are a highly secure moat and cannot be easily breached. A major differentiator for Vijaya is that its radiology services are not solely driven by the basic wellness segment, but by a high volume of specialized work and second opinions.

The B2C advantage: Protecting margins in a competitive landscape

The radiology segment is integrated with other medical fields. Radiologists, cardiologists, medicine specialists, and pathologists work together, constantly communicating to correlate results. This integrated approach significantly reduces waiting times.

This specialization is a key reason why new hubs are growing rapidly and breaking even. It uses a robust tele-radiology system that creates operating leverage by allowing highly specialized doctors to remotely analyze scans and deliver reports to patients in Tier 2/3 locations.

The company recently modernized its capabilities by transitioning to an AI Radiology software named "Augmento." As the company expands its footprint, it actively brings high-end radiology to underserved regions. The B2C business model also allows it to generate a high margin.

9MFY26 financial performance and growth

From a financial perspective, Vijaya's reported double-digit growth. Revenue rose by 17% year-over-year to ₹595 crore in 9MFY26. EBITDA (earnings before interest, taxes, depreciation, and amortization) grew 18% to ₹241 crore, with a margin of 40.6%. Net profit increased 14.8% to ₹125 crore.

Looking ahead, the company aims to expand into large-scale hubs in both core and non-core geographies to drive growth of the radiology business. It is actively bringing advanced, premium radiology equipment to underserved tier-2 and tier-3 markets.

#2 Krsnaa diagnostics: The 70% price discount moat

Krsnaa Diagnostics is one of India’s largest and fastest-growing integrated diagnostic service providers, operating services under a Public-Private Partnership (PPP) framework. Its healthcare infrastructure spans across 18 states and union territories, into tier-II and tier-III towns.

Krsnaa’s presence is spread across the northern region (42%), the western region (34%), and the eastern and southern regions (12% each). The company provides integrated diagnostic services 24/7/365 at prices 50% to 70% lower than prevailing market rates. It is also the only PPP-listed company with a bid-win ratio over 75%.

Discounted Pricing Moat

Source: Krsnaa Investor Presentation

Source: Krsnaa Investor Presentation

Krsnaa operates a massive infrastructure network that includes 190 CT/MRI Centers and 140 pathology labs. It operates 1,501 tele-radiology reporting networks as of Q3FY26. The revenue mix between radiology and pathology is split 50:50.

The Radiology fortress: Higher Capex as a barrier to entry

Unlike typical pathology diagnostic companies, Krsnaa operates a radiology model, with initial equipment investments around 2.5X higher than those of its older peers. This capital-intensive approach reduces short-term return ratios during expansion, but creates a business moat and high barriers to entry that are difficult to replicate.

Maharashtra expansion: 10 new MRI sites to drive Q4FY26 growth

On the radiology expansion front, Krsnaa is actively working on projects in Maharashtra, where 10 new MRI sites are expected to start contributing to revenue from Q4FY26 onwards. A typical radiology project matures over a 5-7-year horizon and delivers organic growth as awareness among local doctors and patients builds.

Rajasthan pivot: Shifting the revenue mix to 70% pathology

Beyond Radiology, the most significant near-term growth driver is the massive pathology rollout in Rajasthan. Once fully operational, management expects the Rajasthan project to contribute around ₹200 crore in annualized revenue by the end of FY27. This will shift the company’s revenue mix to about 65-70% in favour of pathology.

8X retail growth bolsters 28% EBITDA margins

From a financial perspective, Krsnaa Diagnostics reported steady growth in both sales and profit. Revenue grew 9% year-on-year to ₹580 crore in 9MFY26, led by an 8X increase in the retail diagnostic segment revenue. EBITDA grew 13% to ₹160 crore, with a margin of 28%. Net profit increased 5% to ₹59.7 crore.

#3 Suraksha diagnostic: Eastern India’s leader is betting on AI

Suraksha Diagnostic is the largest integrated diagnostic chain in Eastern India, operating under a comprehensive “Hub and Spoke” model to unlock economies of scale. As of 31 December 2025, Suraksha boasts a network of 8 labs, 66 diagnostic centers, and 173 collection centers.

Beyond West Bengal: De-risking via a 100-center regional rollout

Suraksha is primarily based in West Bengal, where it generated 95.5% of its revenue in FY25. To reduce this concentration, it is expanding into neighboring regions, including Bihar, Jharkhand, Assam, and Meghalaya. The company aims to reach 100 centers by FY28, and plans to open 12 to 15 centers annually.

Revenue equilibrium: The balanced radiology and pathology mix

Radiology is a cornerstone of Suraksha operations, acting as a primary revenue driver alongside its pathology business. Pathology accounted for 48% of its revenue in 9MFY26, followed by radiology (46%) and polyclinic (6%). Suraksha’s imaging arsenal includes 16 MRI machines and 29 CT machines.

Suraksha’s Revenue-Mix

Source: Suraksha Investor Presentation

The AI Lever: Adoption of United group Engines for Diagnostic Speed

To increase accuracy and operational efficiency, Suraksha is aggressively integrating advanced IT and AI into its radiology department. The company has recently adopted Artificial Intelligence engines from the United Group, specifically for CT scan and MRI reporting.

Management anticipates that this AI application will act as a growth lever by enabling quicker reporting and improved Turnaround Times for patients. Looking ahead, the company’s future radiology capacity will be driven by its broader target to reach 100 centers by FY28.

Financial Performance: 22% Revenue Jump Anchors 32% EBITDA Margins

From a financial perspective, Suraksha reported steady growth in both sales and profit. Total income grew 22% year-on-year to ₹231 crore in 9MFY26, led by volume expansion from the aggressive rollout of new centers and product mix improvements.

EBITDA grew 13% to ₹73.4 crore, with a margin of 32%. Net profit increased 6% to ₹25.2 crore.Management anticipates that economies of scale will drive margin expansion and improvement starting around Q3 FY27 as the newly added radiology and pathology infrastructure matures.

Valuation Check: Are These Radiology Plays Overpriced?

The return ratios for Vijaya and Suraksha, including return on capital employed (ROCE) and return on equity (ROE), are strong. In terms of valuation, Krsnaa is trading at a much lower multiple than both the industry and historical. Vijaya is trading at a discount to historical but above the industry multiple, while Suraksha is trading close to the industry median.

| Peer Comparison (X) | ||||

| Company | P/E | 3Y Median P/E | ROCE (%) | ROE (%) |

| Vijaya | 55.2 | 66.8 | 20.9 | 19.0 |

| Krsnaa | 21.0 | 32.3 | 12.5 | 9.3 |

| Suraksha | 35.6 | NA | 17.8 | 16.5 |

| Industry Median | 33.6 | – | 22.8 | 17.7 |

Source: Screener.in

Radiology’s shift from a support function to a core revenue driver is reshaping diagnostics. With the market expected to reach ₹62,000 crore and grow at an 11-13% CAGR, organised players with scale and capital are better placed to grow and build durable competitive advantages.

Meanwhile, add them to your watchlist and stay tuned.

Report by The Financial Express

courtesy:Dailyhunt

No comments:

Post a Comment