So far in this Special Situation Series, we’ve covered demergers that are at the closing stages.

With Triveni Engineering the scheme was already sanctioned by the NCLT and the two companies were weeks from trading separately. With Inox Green the demerger was already effective – we were just waiting for shares to land in demat accounts.

Astra Microwave is different. Here we are standing at the starting line, not the finish.

On 27 February 2026, Astra’s board gave only an in-principle approval to demerge its Space, Meteorology and Hydrology business into a separate listed company. The draft Scheme of Arrangement has not even been tabled yet. The board meets on 10 June 2026 to consider it.

There is no share-exchange ratio, no record date, no listing date. Just intent.

That is unusual for this series, and it cuts both ways. You get to think about the situation before the market has fully priced it, but you also have far less certainty: ratios, financials of the carved-out entity, and timelines are all still to come.

What is being spun out, though, is genuinely interesting.

Astra has been a quiet supplier to ISRO – Indian Space Research Organisation for roughly 25 years. When ISRO built the RISAT – Radar-Imaging Satellite, Astra supplied close to 90% of the electronics that went into it. That two-decade relationship, plus a meteorology and hydrology franchise built around Doppler weather radars for the India Meteorological Department (IMD), is what management now wants to have its own ticker.

And note the direction of the cut. Astra is keeping the larger, more mature yet fast growing defence parent and spinning out the smaller, potentially faster-growing space, Meteorology & Hydrology arm

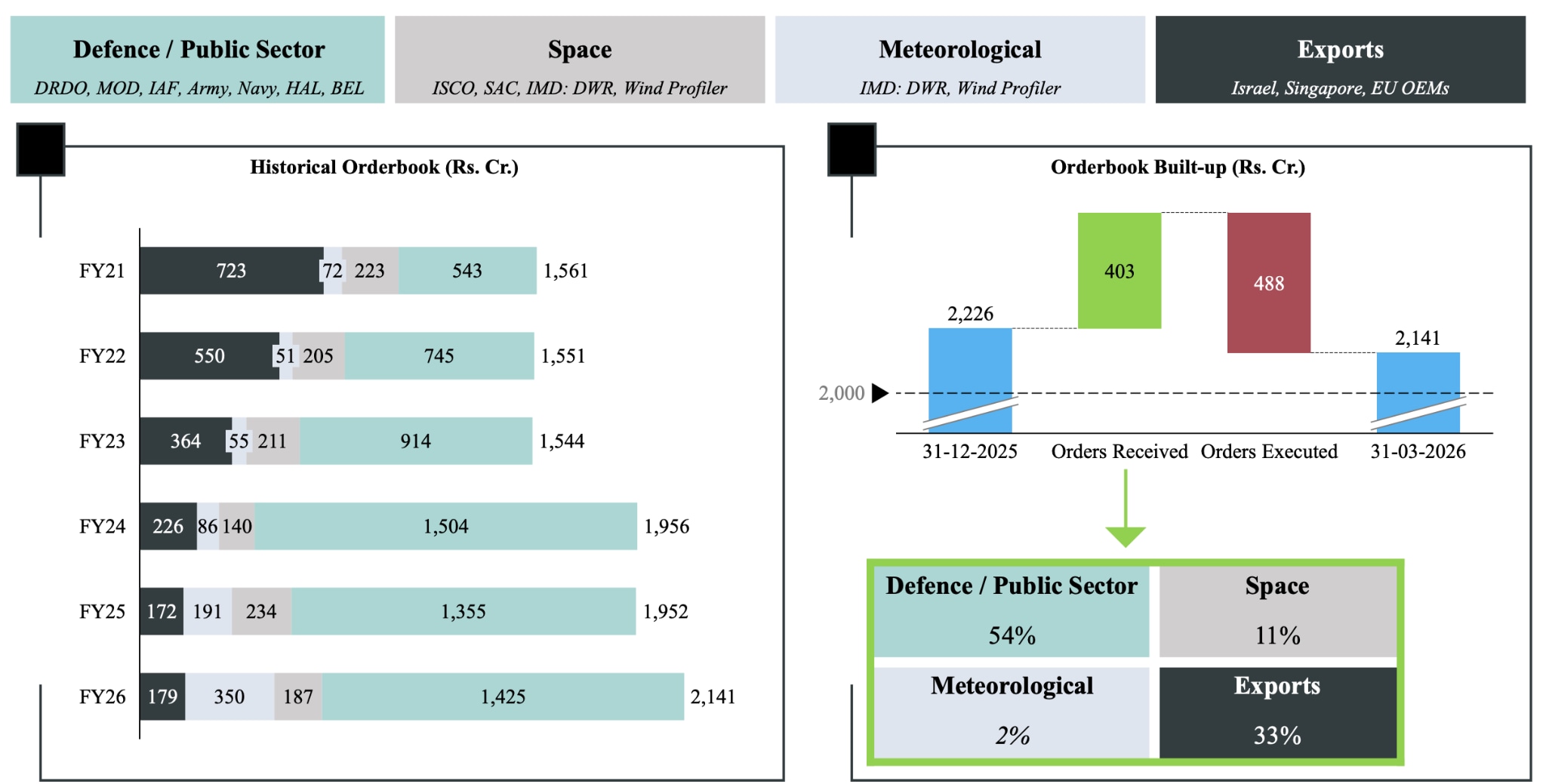

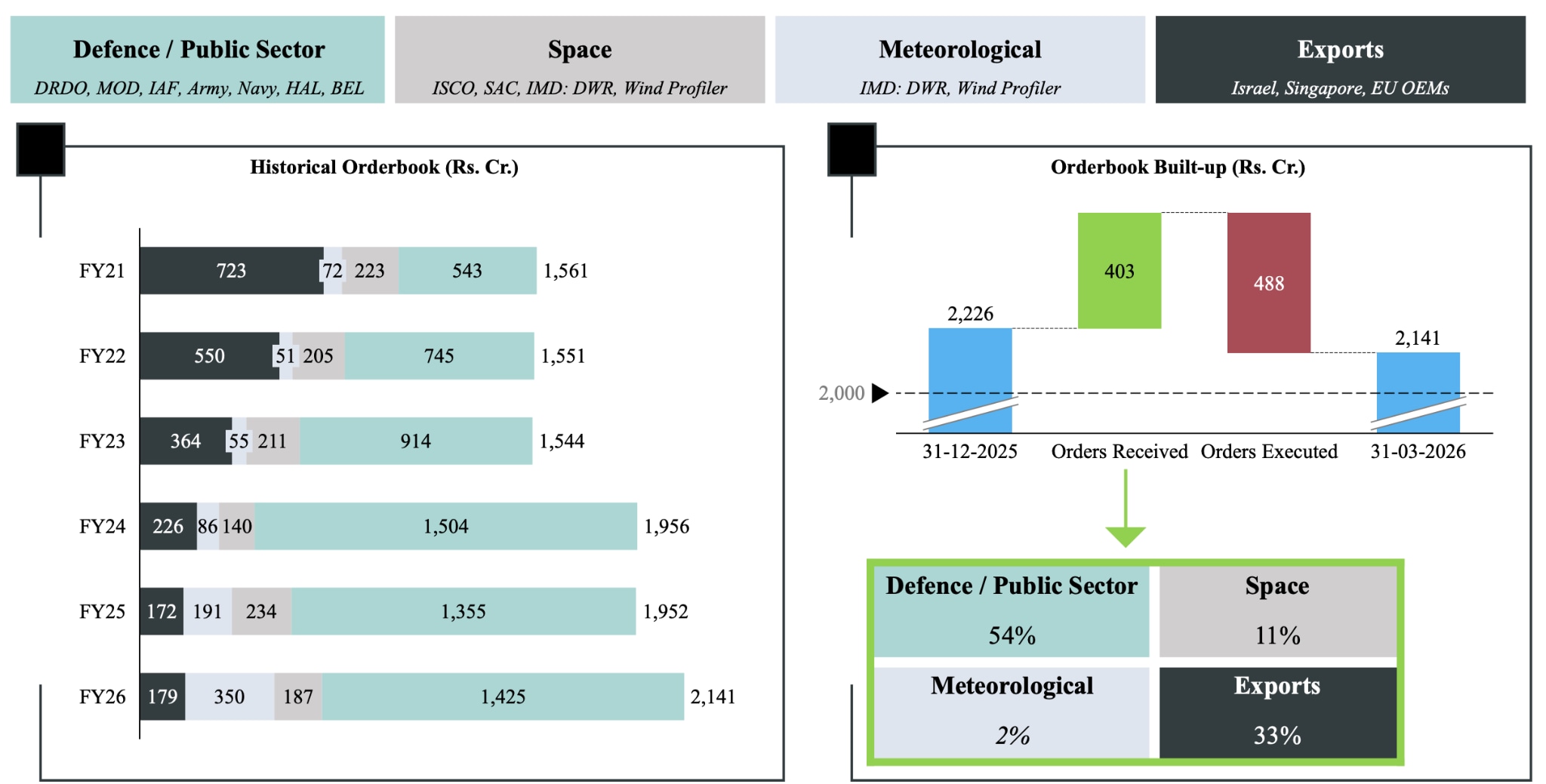

Astra Microwave Order-book Summary (Standalone).

Here is why the move makes sense, what shareholders should eventually receive, where things actually stand, and whether there is value on the table, with the honest caveat that with this one we’re a little early on the demerger timeline.

Why demergers create value

When a single company houses two very different businesses, the market struggles to value it properly.

One business is large, mature and cash-generative. The other is small, fast-growing and full of potential upside. Investors who want the growth engine do not want to pay a growth multiple on the whole company, and investors who want the steady compounder do not want to underwrite a speculative new venture.

So the market splits the difference and assigns one blended multiple. Whichever business is the more exciting one tends to get under-recognised, buried inside the larger entity’s numbers.

This is the conglomerate discount, and a demerger is the standard tool for removing it. Separated, each entity attracts its own investors and analysts, gets its own dedicated management and capital allocation, and pursues its own strategy. The discount tends to fade.

The Indian market has produced a steady run of these.

ITC demerged its hotels business in January 2025, a unit that consumed a large share of capital while contributing only a sliver of profit. ITC Hotels listed separately and ITC became a cleaner FMCG play. Reliance demerged from Jio Financial Services in 2023. Raymond and Aditya Birla Fashion both split contrasting businesses into separate tickers in 2025.

This series has its own reference point. Triveni Engineering demerged its steam-turbine division into Triveni Turbine back in 2010-11. The spun-off entity eventually grew into a company worth more than the parent that birthed it. That is the dream outcome demerger investors chase: a small, high-quality business, given its own identity, re-rating over time into something far larger.

The mechanism works best when the two businesses have genuinely contrasting profiles – different growth rates, different capital needs, different investor bases.

Astra fits that test cleanly: a large, established high growth defence-electronics business on one side, and a smaller, still high-growth space and meteorology franchise on the other.

One honest difference up front. With Triveni and Inox Green, the parent was arguably under-loved and the demerger is expected to remove the discount.

Astra is not “under-loved”. It already trades at a rich multiple (more on that later). So this is less a deep-value, ‘unlock the discount’ story and more a scarcity-and-clarity story i.e – Let a rare, listed NewSpace pure-play find its own multiple, and let the parent stand as a clean defence-electronics business.

Different mechanics, same destination.

Why the Astra demerger makes sense

First, who Astra is.

Astra Microwave Products designs and manufactures high-value RF and microwave components, sub-systems and complete systems for defence, space, meteorology and communications.

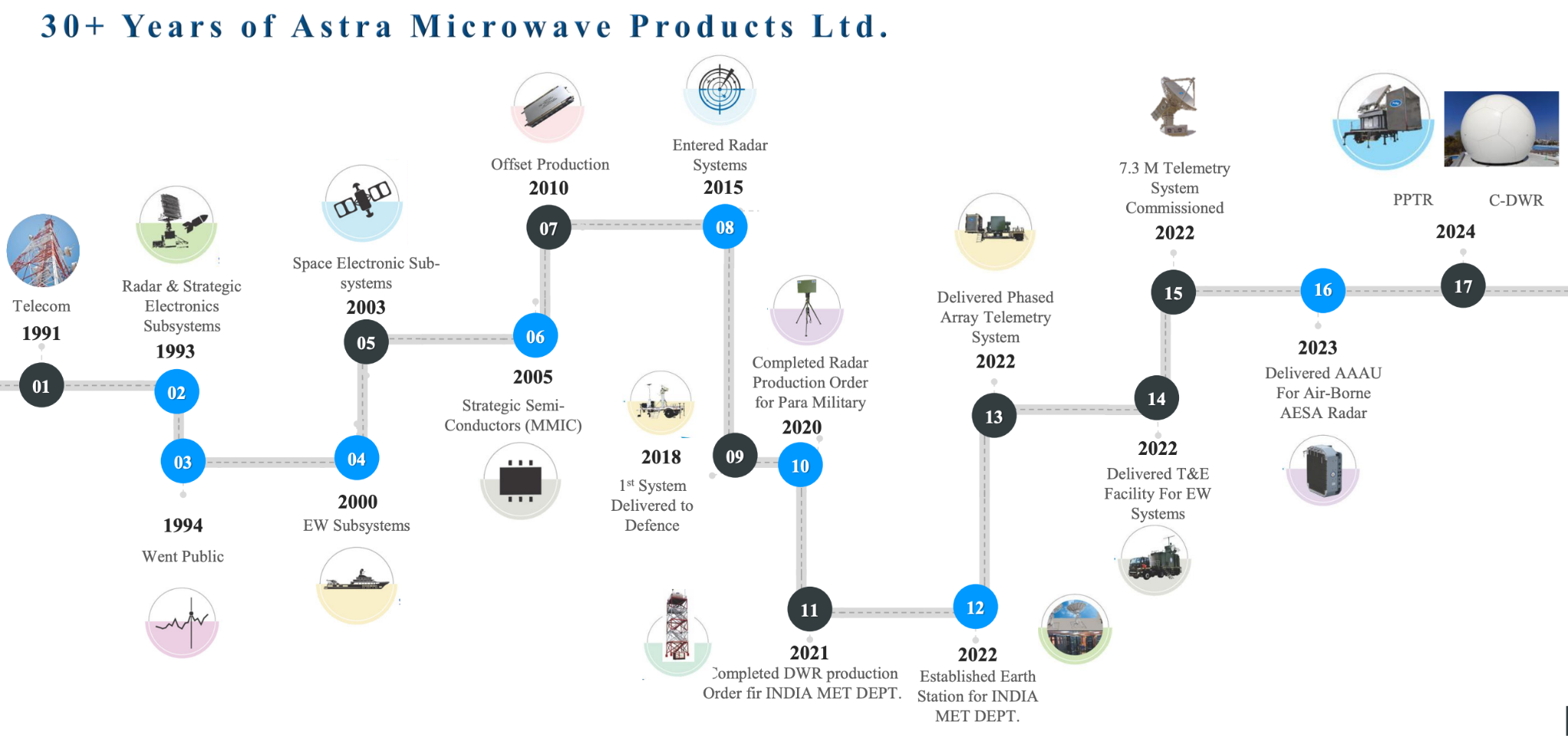

Astra Microwave 30 year Journey

It is one of the few private Indian players of scale in defence electronics, sitting alongside the likes of Bharat Electronics, Data Patterns and Paras Defence, and it supplies radar, electronic-warfare, telemetry and missile electronics to DRDO, BEL, the armed forces and ISRO.

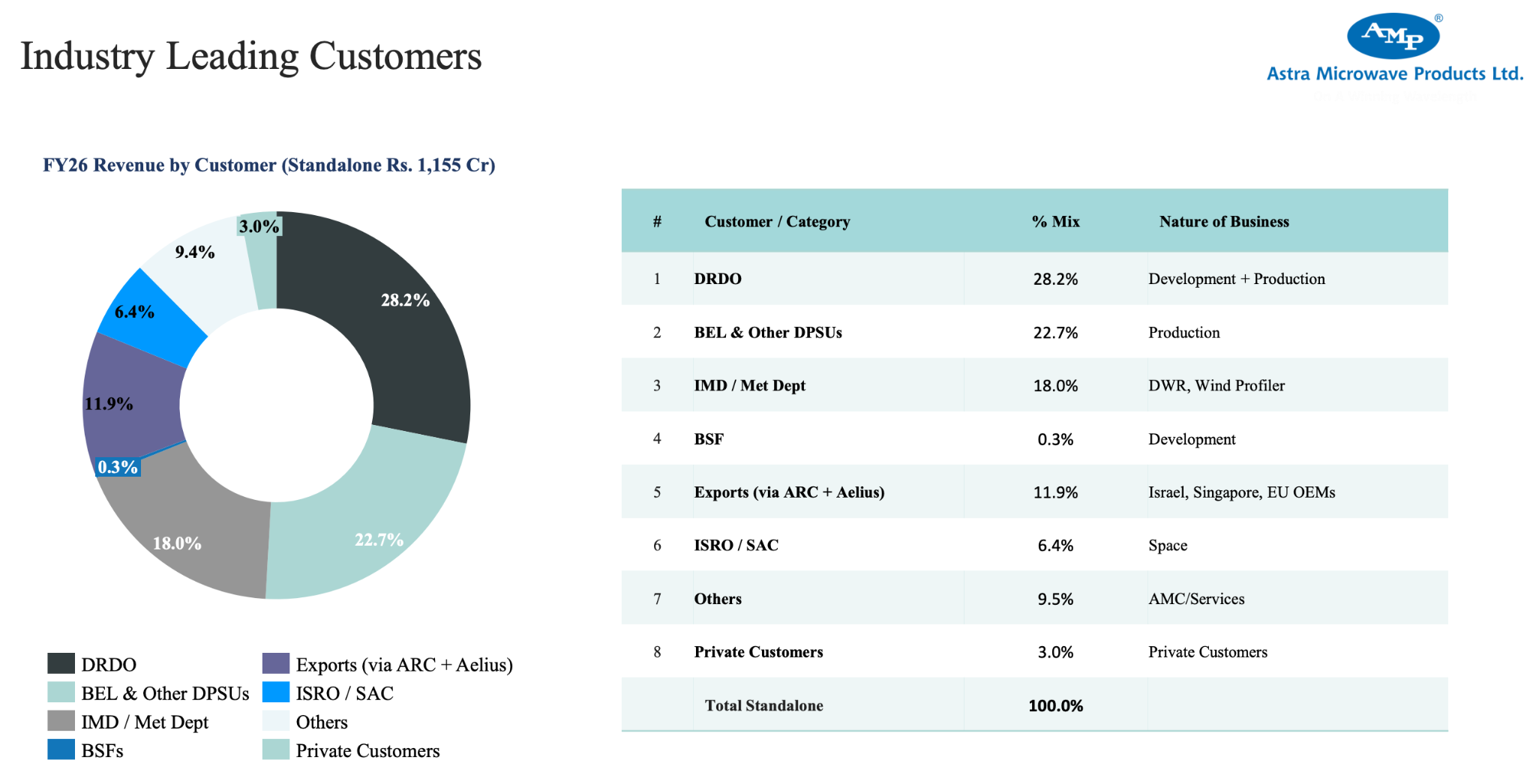

Astra Microwave – customer profile

FY26 was a record year. On a standalone basis, revenue rose 11% to ₹1,156 crore, EBITDA grew 22% to ₹324 crore (a 28.0% margin), and PAT rose 24% to ₹178 crore.

The order book stood at ₹2,141 crore standalone (around ₹2,600 crore consolidated), roughly 1.8x revenue. In December 2025, CRISIL reaffirmed Astra at ‘A’ and revised the outlook to Positive from Stable, a quiet vote of confidence in the cash flows.

The point: the parent is a healthy, profitable, growing defence-electronics company.

This means the demerger is not a rescue operation. It is a focusing exercise.

As for management’s motivation & perspective, here’s what Atim Kabra (Director, Strategy & Business Development) answered to a question about the space opportunity on the Q2 FY26 call:

“Companies are raising money at like $750 million, $800 million valuation with hardly any revenue numbers to their credit. If I extrapolate these numbers, actually, I got close to my current market capitalization. Actually, I have numbers to support that kind of a valuation if I extrapolate space business alone. But forget about that.”

The asset being carved out

Buried inside that defence company is a space and meteorology franchise that has been built patiently over two decades. And it’s starting to grow as well.

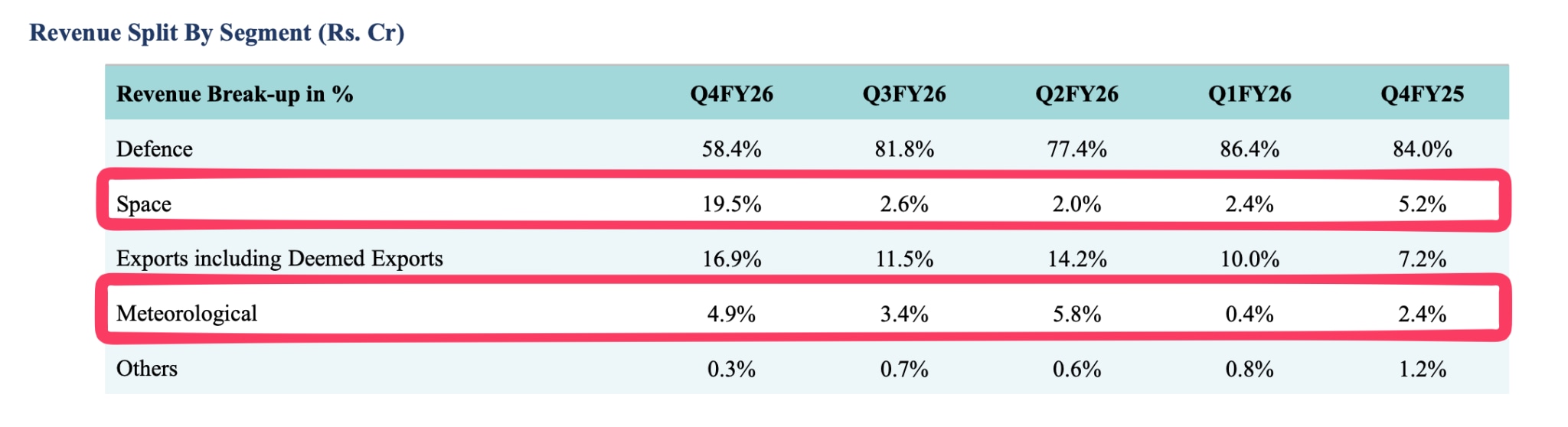

Astra Microwave – Revenue split by segments

- The space heritage is real. Astra first partnered ISRO around 25 years ago, supplied close to 90% of the electronics on the RISAT imaging satellite in 2015, and has cumulatively executed over ₹750 crore of ISRO orders.

- The weather business is a genuine niche. On the meteorology and hydrology side, Astra makes Doppler weather radars and wind profilers for the India Meteorology Department (it delivered ten X-band DWRs to the IMD in 2021) and has cumulatively executed over ₹330 crore of contracts here – a franchise now riding the government’s ‘Mission Mausam’ push.

- The vehicle already exists. Astra has already incorporated Astra Space Technologies Private Limited (ASTPL) as a wholly-owned subsidiary, is recruiting talent, and is building clean rooms for satellite assembly and integration at its Bangalore facility, with the stated aim of launching its own small satellite within two to three years.

In other words, ASTPL is not a shell invented for the scheme. It is an operating, funded effort that the demerger simply formalises and lists.

How big is the space and meteorology business?

This is where the early-stage caveat bites: Astra has not yet published standalone financials for the carved-out entity.

From its disclosures, the space business alone did about ₹110.6 crore of revenue in FY26 with a space order book around ₹187 crore and FY27 order guidance of ₹154 crore.

On the Q4 FY26 call, management put the combined space-and-meteorology contribution at roughly 16% of FY26 revenue, implying something in the region of ₹180–190 crore for the to-be-demerged business, against a defence/radar core that contributes the lion’s share.

Small base, but the right kind of small: high-growth, technology-led, government-and-ISRO-anchored, and exactly the sort of pure-play the market is rewarding generously these days.

The margins still remain a mystery.

Astra discloses no segment margins. Management calls space its highest-margin business, but the demerged entity also carries an equally large meteorology & hydrology book whose margins are undisclosed and likely tender-sensitive, so the carve-out’s true EBITDA margin won’t be known until its first standalone accounts are filed with the scheme

What management says it will unlock

In Managing Director S. Gurunatha Reddy’s words on the Q4 FY26 call: “The objective of this move is to create sharper strategic and operational focus for business segments… enabling dedicated management teams to pursue sector-specific growth opportunities, enhance governance and accountability, simplify the corporate structure, and create clearer investment propositions to shareholders.”

This is no different from the textbook corporate speak we see from most companies undergoing demergers. The underlying is almost always – Unlocking value in either the parent or the spin-off. Unlike in typical cases, Astra’s value unlocking may happen in both entities.

What stays and what goes

| What STAYS in Astra Microwave (AMPL) | What GOES to Astra Space Technologies (ASTPL) |

| Defence & aerospace, exclusively | Space business (~₹110.6 cr FY26 revenue) |

| Radar, EW, telemetry, missile electronics (~bulk of revenue) | Meteorology & hydrology (DWRs, wind profilers) |

| JV stakes: Astra Rafael Comsys (ARC), Navictronics | ~25-year ISRO relationship; satellite integration build-out |

| Wholly-owned defence subsidiaries | Mirror shareholding (same pattern as AMPL) |

| FY27 revenue guidance ₹1,300–1,400 cr | Independent listing targeted on BSE & NSE |

The management hand-off, in context

The leadership change tells you how seriously the company is taking this. Mr. S. Gurunatha Reddy will step down as Managing Director on 30 September 2026, stay on as an Executive Director with the specific charge of overseeing the demerger, and is then expected to join ASTPL as a director effectively going with the business he is carving out.

Dr. M. V. Reddy, currently Joint MD, takes over as MD of AMPL from 1 October 2026.

The growth engine that stays behind

Lest the parent be mistaken for the boring leftover: AMPL is guiding to 15–20% revenue growth in FY27 (₹1,300–1,400 crore), and management has talked about roughly tripling turnover over a 4.5-to-5.5-year horizon, driven by five to six major programs.

Its Astra Rafael Comsys (ARC) JV is expected to cross ₹600 crore of sales in FY27 in additional to the above (₹1,300–1,400 crore), however, since this is a JV – on a consolidated basis only the profit from JV shows up on AMPL’s profit & loss statement.

The bottomline is that both halves of this split are growing, which is precisely why separating them makes sense. It’s so each can be valued on its own terms.

The mechanics and where things stand

Slow down here, because the honest answer to ‘what are the mechanics?’ is: mostly not decided yet. This is the part where Astra differs most from the earlier pieces in this series.

What shareholders should eventually receive

Astra has said ASTPL will have a mirror shareholding pattern as AMPL. In plain terms, every existing Astra shareholder should receive ASTPL shares in proportion to their AMPL holding, with no cash changing hands. You would end up owning two listed companies instead of one: a pure-play defence parent and a pure-play space-and-meteorology spin-off.

While this implies a 1:1 share-exchange ratio, it hasn’t officially been announced yet.

The Audit Committee is to appoint a Registered Valuer, and the final structure, ratio and terms will be decided by the board only after it receives the valuer’s and consultants’ reports.

Until then, exactly how many ASTPL shares you get per AMPL share is unknown and that ratio matters a great deal for how the value is actually distributed.

The path so far, and what’s left

| Milestone | Date | Status |

| In-principle board approval to demerge | 27 Feb 2026 | Done |

| MD transition announced (S.G. Reddy to oversee demerger) | 3 Apr 2026 | Done |

| FY26 results; demerger progress confirmed | 26 May 2026 | Done |

| Q4 FY26 concall – ‘detailed scheme in a few weeks’ | 27 May 2026 | Done |

| Board notice to consider draft Scheme of Arrangement | 1 Jun 2026 | Done |

| Board meeting on draft Scheme (Sec 230–232) | 10 Jun 2026 | Next trigger |

| Registered Valuer report / share-exchange ratio | After board | Awaited |

| Shareholder, creditor, SEBI, exchange & NCLT approvals | Subsequent | Awaited |

| Completion & listing of ASTPL (BSE & NSE) | Target: Q1 FY28 (by ~Jun 2027) | Awaited |

So where are we, really?

At the very beginning. The single most important near-term event is the 10 June 2026 board meeting, where the draft scheme and, hopefully soon after, the all-important share-exchange ratio starts to take shape.

Everything after that (shareholder and creditor approvals, SEBI and exchange no-objections, NCLT sanction) is the long, procedural tail that typically takes a year-plus. Management’s own target is to complete and list ASTPL by Q1 of FY28, i.e. roughly mid-2027.

The valuation math: is there value?

Disclaimer: what follows is a simple, illustrative if-then exercise to help you think about how the market might value these two businesses once they trade separately. It is emphatically not a target price. And because Astra has not yet disclosed ASTPL’s standalone financials or the share ratio, the numbers here are placeholders built on management-stated segment figures — even more provisional than usual.

Start with where the whole sits today

As of early June 2026, Astra trades around ₹1,420 a share, for a market capitalization of roughly ₹13,500 crore.

On trailing FY26 consolidated earnings of ₹193 crore, that is a trailing P/E in the region of 70x.

The stock is near its all-time high (52-week range roughly ₹851–₹1,433) and has run up sharply through 2026 on the defence and demerger themes.

Astra-Microwave Historical

Read that number carefully, because it reframes the whole thesis. At ~70x trailing earnings, Astra is not a cheap, overlooked conglomerate waiting for a discount to unwind. The market is already paying a full, arguably generous multiple for the blended company.

So, the demerger question is not ‘will a hidden discount close?’ It is: ‘can the parts, valued separately, command at least as much as the whole and does the space arm get re-rated to the premium that scarce, listed NewSpace pure-plays enjoy?’

What pure-plays trade at

This is the crux of the bull case. Indian defence-and-space names trade at multiples that look absurd next to most of the market, and the ‘space’ label sits at the very top of that range.

| Listed comparable | What it does | Rough valuation marker (mid-2026) | EV/EBITDA multiples (x) |

| Aerospace & Defence (industry avg) | Sector benchmark | ~44x P/E | 47.6x |

| Astra Microwave (blended, today) | Defence electronics + space/met | ~70x P/E | 37x |

| Paras Defence & Space | Optics, EW, space optics | ~77x P/E | 56x |

| Data Patterns (India) | Defence electronics subsystems | Premium (30–35% growth) | 53.5x |

| MTAR Technologies | Precision eng. — space/nuclear/defence | Premium (high P/E, high sales multiple) | 121x |

The logic writes itself. A clean, listed company whose entire identity is ‘India’s NewSpace + weather-radar pure-play’, anchored by a 25-year ISRO relationship and a satellite-integration build-out, is precisely the kind of scarce asset that domestic and global investors chase.

There is no shortage of money looking for a way to own the India space story. There is a shortage of clean, listed ways to do it.

That scarcity is the re-rating fuel.

The if-then, sketched (and heavily caveated)

If ASTPL carries roughly ₹180–190 crore of FY26 revenue (the ~16% space-and-met figure) and earns at or above the parent’s ~28% EBITDA margin, the trailing EBITDA base is small – perhaps ₹54 – ₹57 crore.

On trailing EBITDA, even a comparable 30X EBITDA multiple makes ASTPL only 10%+ of Astra’s ₹13,500 crore whole.

But pure-play space and defence-electronics names are never valued on trailing earnings, they are valued on Capability, growth and scarcity.

Paras trades near 77x; the cluster sits well above the ~47x sector average.

If the market eventually affords ASTPL a Paras-like premium on a rapidly scaling earnings base (its own satellite, ISRO constellation orders, Mission Mausam radar demand), the spun-off entity could be worth a multiple of its trailing profit – the question is simply how many years of growth the market is willing to pay for on day one.

The bear case is equally simple. First, the parent is already expensive, so a chunk of any ‘pure-play premium’ may already be embedded in Astra’s 70x.

Second, the carved-out base is genuinely small and lumpy – space and meteorology revenue swings quarter to quarter (space was 19.5% of revenue in Q4 FY26 but ~2–3% in earlier quarters), and order flow depends on ISRO and government cycles.

Third, and most importantly, none of the terms are set: an unfavourable share-exchange ratio, holding-company-style discounts, or a slow NCLT process could all blunt the outcome.

Pulling it together

The case here is not a tidy sum-of-the-parts that screams mispricing on day one. The parent is too richly valued for that.

The case is optionality. You have a healthy, growing defence-electronics business that will emerge as a clean pure-play, plus a free, attached call option on a scarce listed NewSpace asset that the market may eventually value far above its trailing earnings.

What makes Astra worth watching is the timing.

With Triveni and Inox Green, the work was nearly done by the time the story was clear. Here, the scheme has not even been tabled, the share swap ratio isn’t set, we’re at least about 12 months from the actual demerger.

That is more risk and more room to think.

The single most important thing to watch is the 10 June 2026 board meeting and the share-exchange ratio that follows. As management itself frames it, the aim is to ‘create sharper strategic and operational focus’ and unlock value over the medium to long term.

The point of a demerger is rarely that the math works on day one. It is that a focused, scarce business, given its own identity and its own investor base, tends to find a better multiple over time than it ever could while buried inside its parent.

Note: We have relied on company filings (the FY25 Annual Report, quarterly investor presentations and con-call transcripts, the 27 February 2026 demerger press release, and the December 2025 CRISIL rating rationale) and on widely used market-data sources for price and market-cap figures throughout this article. Where a figure is an author calculation built on management-guided or segment numbers, it is marked as such. Because the demerger is at an early, in-principle stage, the share-exchange ratio and the carved-out entity’s standalone financials are not yet available.

Source: FinancialExpress

Disclaimer:

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

Disclosure: The writer or his dependents do NOT hold shares in the securities/stocks/bonds discussed in this article. the articles and the interpretation of data are solely the personal views of the contributors/writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.

No comments:

Post a Comment