The market reversed some of previous week's gains and fell around 1 percent amid a global sell off triggered by escalating concerns over AI related disruptions which led to sharp selling in IT stocks. This, combined with geopolitical tensions, significantly weighed on market breadth, causing the earlier optimism to fade and prompting a widespread selling pressure. However, the week was opened on a firm note, supported by favourable trade deal developments and renewed FII inflows that lifted overall risk appetite.

But in between, overall, the market traded in the previous week's range. Hence, the consolidation with range-bound trading may be seen in the upcoming week starting from February 16, though the caution prevails with focus on global AI driven distruptions. The market will closely watch flash PMI readings, FOMC minutes, US advance GDP numbers, and FIIs mood next week.The Nifty 50 declined 223 points (0.87 percent) to 25,471, and the BSE Sensex shed 954 points (1.14 percent) to 82,627, while the broader markets outperformed benchmark indices as the Nifty Midcap100 index fell 0.11 percent and Smallcap 100 index gained 0.56 percent during the week passing by.

"In the near term, with tariff related concerns easing and the domestic earnings season

drawing to a close on a mixed trend, market focus will hinge largely on global cues, including the US labour data and shifting

expectations surrounding the US Fed's policy path," Vinod Nair, Head of Research at Geojit Investments said.

According to him, with IT and metals facing persistent structural and external headwinds, market leadership may rotate toward domestically oriented sectors such as banking, autos, and select consumption driven segments.Further, Ajit Mishra – SVP, Research at Religare Broking feels the coming week includes important domestic macro releases that could influence near-term sentiment. "Markets will monitor WPI inflation and Balance of Trade data for signals on price trends and external sector dynamics. High-frequency indicators due include HSBC flash PMI readings for Manufacturing, and Services, along with bank loan growth and foreign exchange reserves data. These releases will be evaluated for confirmation of growth momentum amid volatile global cues and continued repricing in technology stocks."

However, the overall sentiment is likely to remain cautious as investors monitor global AI driven disruptions and geopolitical risks while improved valuations and constructive GDP forecasts may help sustain FII inflows, he added.

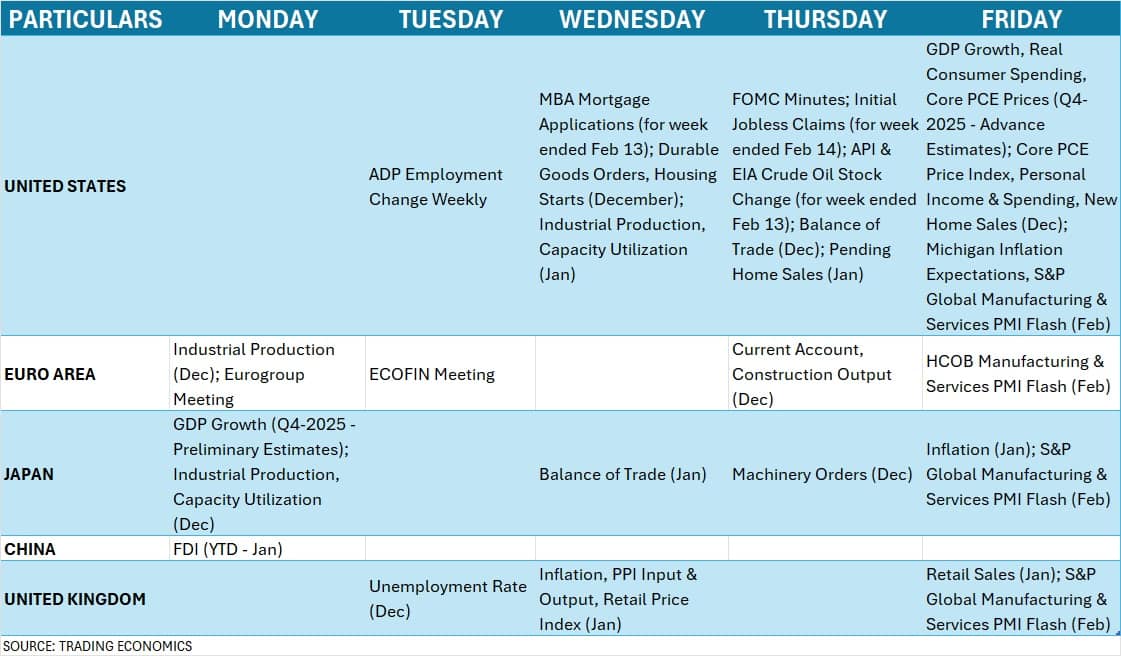

Here are 10 key factors to watch next week:FOMC MinutesGlobally, the market participants across asset classes will focus on the Federal Reserve's preferred inflation gauge, the Personal Consumption Expenditures (PCE) Price Index, due on February 19 and 20, respectively. The softer reading could pull forward rate-cut expectations to June from the current July pricing, according to experts.In addition, FOMC meeting minutes, US advance GDP data for December 2025 quarter, and weekly jobs numbers will also be closely monitored. According to most economists, the economic growth for Q4-CY25 is expected to be lower compared to 4.4 percent seen in previous quarter (Q3).Global Economic DataFurther, the focus will also be on the flash PMI readings for February from major global economies including United States, Japan, United Kingdom, and also Europe.The participants will also keep an eye on the preliminary estimates for Japan's GDP growth in Q4-2025 and country's inflation numbers for January due on February 16 and 20, respectively. Further, unemployment rate for December, and inflation & retail sales for January from United Kingdom will also be watched next week.

The week ahead will be holiday-shortened as US markets will be closed for Presidents' Day on February 16, and Chinese exchanges remain shut until February 23 for the Lunar New Year.SC's ruling on Trump tariffsMarkets will also watch the Supreme Court's ruling on Donald Trump tariffs scheduled for February 20. US President Donald Trump started of levying duties on all goods and services entering the country along with reciprocal tariffs on select countries since April 2025. Since then, the White House has been negotiating with its trading partners.Last November, the Supreme Court heard oral arguments challenging the auspices under which Trump justified the tariffs. The decision was expected in January. The high court hasn't ruled yet, and there's concern in the White House that a negative ruling could force the US into reimbursing the duties collected so far. The tariffs helped put a dent in the pace of the budget deficit. Customs duties collected through tariffs totalled $30 billion for the month, putting the fiscal year-to-date tally at $124 billion, or 304% more than the same period in 2025. CNBC-TV18 reported.Domestic Economic DataBack home, the market participants will focus on the WPI inflation data for January due on February 16 which most economists feel is expected to climb over 1 percent compared to 0.83 percent in previous month.The unemployment rate and balance of trade numbers for January will also release on the same day. Unemployment rate is expected to be around similar levels of previous month.Further, HSBC manufacturing and services PMI flash data for February as well as bank loan & deposit growth for fortnight ended February 6 and foreign exchange reserves for week ended February 13 will be released on final day of next week i.e. February 20. Manufacturing PMI in January rose to 55.4 (against 55 in December), while services PMI also climbed to 58.5 (from 58) in the same period.FII FlowThe focus wlll also be on the FIIs (Foreign Institutional Investors) mood check as they turned out to be significant sellers on Friday to the tune of Rs 7,395 crore which resulted in to the net outflow not only for last week (Rs 4,019 crore) but also for February (Rs 1,374 crore). Before Friday's outflow, they were net buyers for the week as well as current month in the cash segment.On the contrary, DIIs (Domestic Institutional Investors) maintained their support to the equity market, fully compensating the FIIs outflow in the week and month. They net bought Rs 6,884 crore worth shares during the week, and Rs 9,776 crore in the month.Meanwhile, the Indian rupee appreciated for second consecutive week, strengthening 0.06 percent to 90.5 against the US dollar amid throughout the week consolidation, in addition to 1.19 percent rally in previous week.IPOOn the primary market front, investors will see total three IPOs - Gaudium IVF & Women Health, Fractal Industries, and Yashhtej Industries (India) - next week. Of which, fertility services provider Gaudium IVF & Women Health will be the only IPO from the mainboard segment, opening for subscription on February 20, while others two are from the SME segment - Fractal Industries, and Yashhtej Industries which will open on February 16 and 18, respectively.Marushika Technology, the SME IPO, will remain open till February 16, while its shares will be available for trading on the NSE Emerge effective February 19.Mainboard companies - Fractal Analytics, and Aye Finance will make their market debut on February 16.Technical ViewTechnically, the Nifty faced lot of resistance at the psychological 26,000 zone and decisively closed below the same during the week. It slipped below short term moving averages as well as midline of Bollinger bands with above-average volumes, while the momentum indicators are not supportive either. For the upcoming week, the index is expected to be in 25,300-26,000 range as convincing trade above it can open door for record high (26,373) or below it the fall toward 25,000 can't be ruled out.F&O CuesThe weekly options data suggested that the 25,600 is expected to be immediate resistance for the Nifty 50 followed by the 25,900-26,000, with support at 25,300 followed by 25,000 being a crucial support zone.The maximum Call open interest was seen at the 26,000 strike, followed by the 25,600 and 25,900 strikes, with the maximum Call writing at the 25,600, 25,500 and 25,700 strikes. On the Put side, the 25,000 strike holds the maximum Put open interest, followed by the 25,500 and 25,300 strikes, with the maximum Put writing at the 25,000, 25,300 and 25,400 strikes.India VIXMeanwhile, the fear gauge, India VIX needs to decisively fall below 11.5 zone for the bulls to get in to comfort zone, until then the caution is expected to prevail in the market. The VIX spiked 11.33 percent during the week to 13.29 after a 20.9 percent decline in previous week.

The week ahead will be holiday-shortened as US markets will be closed for Presidents' Day on February 16, and Chinese exchanges remain shut until February 23 for the Lunar New Year.SC's ruling on Trump tariffsMarkets will also watch the Supreme Court's ruling on Donald Trump tariffs scheduled for February 20. US President Donald Trump started of levying duties on all goods and services entering the country along with reciprocal tariffs on select countries since April 2025. Since then, the White House has been negotiating with its trading partners.Last November, the Supreme Court heard oral arguments challenging the auspices under which Trump justified the tariffs. The decision was expected in January. The high court hasn't ruled yet, and there's concern in the White House that a negative ruling could force the US into reimbursing the duties collected so far. The tariffs helped put a dent in the pace of the budget deficit. Customs duties collected through tariffs totalled $30 billion for the month, putting the fiscal year-to-date tally at $124 billion, or 304% more than the same period in 2025. CNBC-TV18 reported.Domestic Economic DataBack home, the market participants will focus on the WPI inflation data for January due on February 16 which most economists feel is expected to climb over 1 percent compared to 0.83 percent in previous month.The unemployment rate and balance of trade numbers for January will also release on the same day. Unemployment rate is expected to be around similar levels of previous month.Further, HSBC manufacturing and services PMI flash data for February as well as bank loan & deposit growth for fortnight ended February 6 and foreign exchange reserves for week ended February 13 will be released on final day of next week i.e. February 20. Manufacturing PMI in January rose to 55.4 (against 55 in December), while services PMI also climbed to 58.5 (from 58) in the same period.FII FlowThe focus wlll also be on the FIIs (Foreign Institutional Investors) mood check as they turned out to be significant sellers on Friday to the tune of Rs 7,395 crore which resulted in to the net outflow not only for last week (Rs 4,019 crore) but also for February (Rs 1,374 crore). Before Friday's outflow, they were net buyers for the week as well as current month in the cash segment.On the contrary, DIIs (Domestic Institutional Investors) maintained their support to the equity market, fully compensating the FIIs outflow in the week and month. They net bought Rs 6,884 crore worth shares during the week, and Rs 9,776 crore in the month.Meanwhile, the Indian rupee appreciated for second consecutive week, strengthening 0.06 percent to 90.5 against the US dollar amid throughout the week consolidation, in addition to 1.19 percent rally in previous week.IPOOn the primary market front, investors will see total three IPOs - Gaudium IVF & Women Health, Fractal Industries, and Yashhtej Industries (India) - next week. Of which, fertility services provider Gaudium IVF & Women Health will be the only IPO from the mainboard segment, opening for subscription on February 20, while others two are from the SME segment - Fractal Industries, and Yashhtej Industries which will open on February 16 and 18, respectively.Marushika Technology, the SME IPO, will remain open till February 16, while its shares will be available for trading on the NSE Emerge effective February 19.Mainboard companies - Fractal Analytics, and Aye Finance will make their market debut on February 16.Technical ViewTechnically, the Nifty faced lot of resistance at the psychological 26,000 zone and decisively closed below the same during the week. It slipped below short term moving averages as well as midline of Bollinger bands with above-average volumes, while the momentum indicators are not supportive either. For the upcoming week, the index is expected to be in 25,300-26,000 range as convincing trade above it can open door for record high (26,373) or below it the fall toward 25,000 can't be ruled out.F&O CuesThe weekly options data suggested that the 25,600 is expected to be immediate resistance for the Nifty 50 followed by the 25,900-26,000, with support at 25,300 followed by 25,000 being a crucial support zone.The maximum Call open interest was seen at the 26,000 strike, followed by the 25,600 and 25,900 strikes, with the maximum Call writing at the 25,600, 25,500 and 25,700 strikes. On the Put side, the 25,000 strike holds the maximum Put open interest, followed by the 25,500 and 25,300 strikes, with the maximum Put writing at the 25,000, 25,300 and 25,400 strikes.India VIXMeanwhile, the fear gauge, India VIX needs to decisively fall below 11.5 zone for the bulls to get in to comfort zone, until then the caution is expected to prevail in the market. The VIX spiked 11.33 percent during the week to 13.29 after a 20.9 percent decline in previous week. Report by Sunil Shankar Matkar at Moneycontrol

No comments:

Post a Comment